Recent copper price fluctuations have intensified slightly compared to Q2, with two waves of jumps initially and then pull backs occurring in late June and late July. The first rally was primarily driven by the sustained weakening of the US dollar index and continuous inventory drawdowns in non-US regions, while the second was boosted by domestic anti-"rat race" sentiment. Why have the recent copper price rallies been difficult to sustain? What risks should the copper market watch as the critical tariff period approaches?

Global Trade Relations Ease, Limited Boost from Anti-"Rat Race" Sentiment

Trade negotiations between the US and other countries continue after the tariff suspension period. As the market had already digested the reciprocal tariffs announced in early April, concerns over economic prospects did not escalate further during this round of talks. Recently, the US high-profile announced trade agreements with Japan, the Philippines, and others, while tensions with the EU shifted toward easing, culminating in an overall framework agreement last Sunday, reducing tariff-related uncertainties. The latest China-US economic and trade talks in Stockholm concluded recently, with both sides agreeing to extend the suspended 24% US reciprocal tariffs and China's countermeasures as scheduled, while maintaining close communication between their trade teams. This outcome aligned with market expectations, further weakening risk-off sentiment.

Expectations and policies related to anti-"rat race" measures continued to ferment, coupled with growing calls for industry self-discipline, fueling a surge in related industrial products and significantly boosting optimism in futures markets. SHFE copper prices also saw temporary support. Although the MIIT's key industry growth stabilization plan included non-ferrous metals, only alumina reacted strongly within the sector. Copper's brief strength was more sentiment-driven, with relatively mediocre performance. The reasons: first, US import copper tariff policies this year diverted global copper flows to the US, keeping domestic copper inventories persistently low and alleviating surplus concerns. Second, COMEX copper's early rally and low inventory provided strong price support, keeping SHFE copper hovering near multi-year highs without significant low-price correction needs. Additionally, amid ongoing tight copper concentrate supply and increasing smelter production pressure, the "High-Quality Development Implementation Plan for the Copper Industry (2025-2027)" was jointly issued by the MIIT and 10 other departments in February. The plan outlines key tasks including resource security, technological innovation, structural adjustment, and green-smart transformation. Regarding capacity, it mandates new smelting projects to include proportional equity copper concentrate capacity, effectively tightening new smelting capacity. As the market had already priced this in, copper prices showed limited reaction without further supply tightening signals.

Short-term Copper Ore Supply Tightness Unlikely to Ease, Smelter Response Remains Key

Following the mid-year negotiations between domestic smelters and Antofagasta, which set the copper concentrate processing fee for next year at zero, CSPT did not set a guidance price for spot copper concentrate processing fees in Q3. Although the recent spot copper concentrate processing fees in China have shown signs of stabilization, the rebound has been very limited. Various signs indicate that the tight supply situation of domestic copper concentrates is difficult to alleviate, and the bargaining power of miners has increased. According to the overseas copper miner production disclosures in Q2 this year, Rio Tinto and Vale increased their production in Q2. However, Teck Resources cut its full-year copper production target, and Kamoa-Kakula, affected by the earthquake, also lowered its production guidance for copper this year. The growth rate of global copper ore supply remains not optimistic.

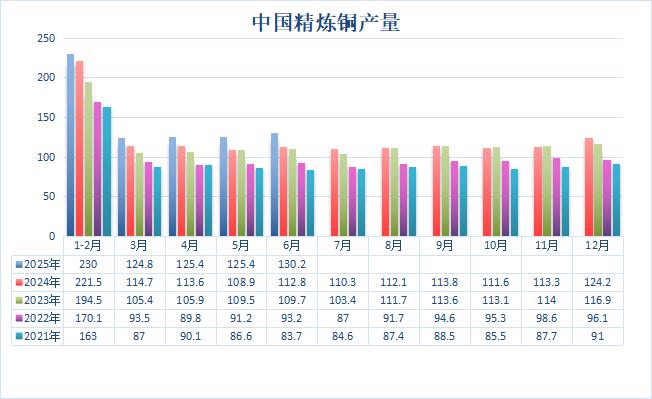

Domestic smelters have been facing the dilemma of extremely low spot processing fees for a long time. However, due to the strong performance of by-products such as sulphuric acid and gold, which have brought additional profits, combined with the majority of acceptable long-term contract processing fees, the refined copper production announced by the National Bureau of Statistics in H1 showed a steady increase, up 9.5% compared to the same period last year. Against the backdrop of no reduction in smelting output, the support of ore supply tightness for copper prices is relatively limited. In July, domestic smelters had fewer maintenance periods, and the capacity utilization rate of newly commissioned smelters continued to rise. The market's concern about large-scale production cuts by enterprises due to losses did not materialize. SMM believes that there is still an expectation for an increase in domestic copper cathode production. However, the long-term contract processing fees negotiated by smelters and miners this year are significantly lower, and even fell to negative values in the early negotiations in mid-year. The pressure faced by smelters will become increasingly severe, and it is still necessary to pay attention to the smelter operation situation in the future.

The US Copper Taxation Period May Be Approaching, Global Copper Trade Pattern Begins to Shift

This month, the statements of US officials regarding import copper tariffs have shocked the global copper market, mainly due to the significant increase in the proposed tariff rate on copper imports by the US, surging from the previously expected 25% to 50%. At the same time, the implementation period has also been advanced from the expected September-October to August 1st. After the news was released, COMEX copper continued to surge sharply, but LME copper and SHFE copper showed a pullback. The LME copper 0-3 price spread also quickly shifted from a premium to a discount, with the underlying logic being market concerns that the rapid implementation of import copper tariffs would reverse the trade situation of global copper flowing into the US, leading to an increase in copper inventories in non-US regions. Since July, LME copper inventories have indeed reversed the previous de-stocking trend and shown a continuous accumulation, with LME copper inventories rising from around 90,000 mt previously to over 127,000 mt currently in just one month, indicating that some cargoes were indeed unable to be shipped to the US in time and chose to be transferred to LME delivery warehouses. Recently, the US has been busy with trade negotiations with other countries and has reached agreements one after another, without making further statements on the tariff hikes for imported copper. As the original deadline of August 1 approaches, if the tariff hikes are indeed implemented as scheduled and no countries are exempted, given that the US copper imports exceeded 500,000 mt in H1 and the recent window period remains open, the US's annual copper demand will be basically met. Faced with high tariffs and high import costs, domestic demand for copper in the US will weaken, and more copper flowing into consumption areas needs to be guarded against in the future.

Recently, the rebound in copper prices has not exceeded the highs set in early July, and the reaction to positive sentiment has been relatively small, with futures prices quickly returning to the previous range of fluctuations. The reason is that although domestic social inventory of copper remains at a low level and difficult to accumulate due to the US's siphoning effect on global copper, the real consumption in the copper market is still constrained by the off-season demand, while ore supply tightness and profit pressures have not yet caused a decline in smelting operations, making it difficult for the supply and demand front to bring more upward momentum.

Recently, the US's trade negotiations with various countries are in full swing, and the market's overall concerns about the early stage of the economy have eased. The IMF has slightly raised its global economic growth forecasts for this year and next, and is more optimistic about China's economic prospects. Coupled with the support of "anti-rat race competition sentiment," the macro front atmosphere is moderate. August 1 is an important period related to the US's tariff hikes on copper. As the market has already anticipated this, if the tariff hikes are indeed implemented as scheduled, there may be an increase in copper price fluctuations on that day. However, under the premise that inventory in non-US regions has not temporarily seen a significant increase, there is still support below copper prices.

(Wenhua Comprehensive)